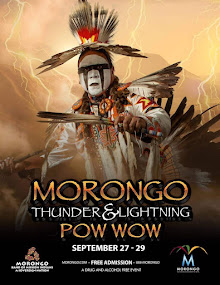

PHOTOS. A Chinese investor at a stock price board at a private security firm in Shanghai on October 6. World stock markets have plummeted, striking four-year lows, as panic-stricken investors doubted whether a Wall Street bailout package would stem the global financial crisis (AFP/Mark Ralston).

TOKYO (AFP) -- World stock markets plunged again Tuesday as the global financial crisis deepened, with governments taking emergency measures to shore up confidence but failing to stem the panic.

Markets in Asia opened sharply down, with shares in Tokyo falling more than five percent at one point, a day after a global rout saw New York's Dow Jones Industrial Average fall below 10,000 points for the first time since 2004.

In Washington, Treasury officials said they would act quickly to implement a massive bailout plan for the financial sector, seeking bids by Wednesday to manage the troubled mortgage-related assets at the root of the crisis.

The Federal Reserve and Treasury said they were studying the possibility of making unsecured loans in an effort to keep much-needed credit flowing.

In Europe, finance ministers were to begin preparing their first joint measure Tuesday to reassure nervous savers by ramping up minimum bank deposit guarantees.

In a joint declaration Monday they pledged to protect the stability of financial institutions by providing "liquidity support through central banks, action to deal with individual banks or enhanced depositor protection schemes."

The Luxembourg meeting could produce the first joint European response to the financial crisis in the form of a plan to lift minimum bank deposit guarantees to as much as 100,000 euros (135,000 dollars).

"We will all take the necessary measures to ensure the stability of the financial system," said Jean-Claude Juncker, who heads the group of finance ministers from the 15 countries that share the euro.

Jean-Claude Trichet, president of the European Central Bank, said the ECB would keep injecting money into the banking system "as long as necessary" to help institutions hit by the current crisis.

The Federal Reserve meanwhile said it would start to pay interest on bank deposits and expand bank loans to up to 900 billion dollars by year-end in a bid to increase liquidity.

President George W. Bush visited a group of small business owners in Texas, saying he understood the difficulties being faced by the car dealer, auto shop repair owner and restaurateurs he had met.

"It's clear they're dealing with the effects of a credit crunch," Bush said. "They're having trouble getting money to be able to continue to expand their business or money to help their consumers be able to buy their products."

The turmoil emerged after the collapse of loans to would-be US homebuyers with shaky credit histories and caused a chaotic chain reaction, revealing how cheap credit throughout the financial system had created a massive bubble.

The US government approved a law Friday to buy up 700 billion dollars of bad mortgages and other assets from banks, which would wipe the debts from their books in hopes they will be able to start lending more freely again.

But approval of the massive bailout plan has failed to calm world markets, which have continued to tumble sharply. Economist Peter Morici at the University of Maryland said the bailout had not worked.

"The bank bailout will provide banks with much-needed liquidity but it does not address the compensation and management practices on Wall Street that drove irresponsible decisions and gave rise to the crisis," he said.

Shares in Tokyo were down 3.10% at the end of the morning session Tuesday, recovering some of the Nikkei's losses earlier in the session.

On Monday, Wall Street came back from the edge, with the Dow Jones Industrial Average closing down 3.58%, off 369 points after losing as much as 800 points.

The partial comeback offered a glimmer of hope on an otherwise horrific day for global markets that saw London's FTSE 100 index fall 7.86% and Paris's CAC 40 shed 9.04%.

Shares in Moscow fell 19.10%, the market's worst-ever tumble.

"When will the slide end? It's anybody's guess," said David Kastner at Charles Schwab & Co.

"But the aggressive actions being taken by the Fed, and increasingly by the central bankers in Europe and Asia, point to an eventual stabilization in confidence -- where the real crisis lies. In the meantime, we expect sharp bouts of bargain hunting and more panic sell-offs."

In Iceland, Prime Minister Geir Haarde said the government was ready to take control of the country's banks, citing "a gargantuan crisis which is part of a broader worldwide crisis."

After a weekend summit of the European Union's big four leaders in Paris, member states' leaders issued a joint statement on Monday vowing to defend banks while remaining divided on a US-style bailout fund.

The turbulence pushed the euro down against the dollar and yen, while oil prices fell below 90 dollars a barrel on fears about slowing demand for energy.

Markets in Asia opened sharply down, with shares in Tokyo falling more than five percent at one point, a day after a global rout saw New York's Dow Jones Industrial Average fall below 10,000 points for the first time since 2004.

In Washington, Treasury officials said they would act quickly to implement a massive bailout plan for the financial sector, seeking bids by Wednesday to manage the troubled mortgage-related assets at the root of the crisis.

The Federal Reserve and Treasury said they were studying the possibility of making unsecured loans in an effort to keep much-needed credit flowing.

In Europe, finance ministers were to begin preparing their first joint measure Tuesday to reassure nervous savers by ramping up minimum bank deposit guarantees.

In a joint declaration Monday they pledged to protect the stability of financial institutions by providing "liquidity support through central banks, action to deal with individual banks or enhanced depositor protection schemes."

The Luxembourg meeting could produce the first joint European response to the financial crisis in the form of a plan to lift minimum bank deposit guarantees to as much as 100,000 euros (135,000 dollars).

"We will all take the necessary measures to ensure the stability of the financial system," said Jean-Claude Juncker, who heads the group of finance ministers from the 15 countries that share the euro.

Jean-Claude Trichet, president of the European Central Bank, said the ECB would keep injecting money into the banking system "as long as necessary" to help institutions hit by the current crisis.

The Federal Reserve meanwhile said it would start to pay interest on bank deposits and expand bank loans to up to 900 billion dollars by year-end in a bid to increase liquidity.

President George W. Bush visited a group of small business owners in Texas, saying he understood the difficulties being faced by the car dealer, auto shop repair owner and restaurateurs he had met.

"It's clear they're dealing with the effects of a credit crunch," Bush said. "They're having trouble getting money to be able to continue to expand their business or money to help their consumers be able to buy their products."

The turmoil emerged after the collapse of loans to would-be US homebuyers with shaky credit histories and caused a chaotic chain reaction, revealing how cheap credit throughout the financial system had created a massive bubble.

The US government approved a law Friday to buy up 700 billion dollars of bad mortgages and other assets from banks, which would wipe the debts from their books in hopes they will be able to start lending more freely again.

But approval of the massive bailout plan has failed to calm world markets, which have continued to tumble sharply. Economist Peter Morici at the University of Maryland said the bailout had not worked.

"The bank bailout will provide banks with much-needed liquidity but it does not address the compensation and management practices on Wall Street that drove irresponsible decisions and gave rise to the crisis," he said.

Shares in Tokyo were down 3.10% at the end of the morning session Tuesday, recovering some of the Nikkei's losses earlier in the session.

On Monday, Wall Street came back from the edge, with the Dow Jones Industrial Average closing down 3.58%, off 369 points after losing as much as 800 points.

The partial comeback offered a glimmer of hope on an otherwise horrific day for global markets that saw London's FTSE 100 index fall 7.86% and Paris's CAC 40 shed 9.04%.

Shares in Moscow fell 19.10%, the market's worst-ever tumble.

"When will the slide end? It's anybody's guess," said David Kastner at Charles Schwab & Co.

"But the aggressive actions being taken by the Fed, and increasingly by the central bankers in Europe and Asia, point to an eventual stabilization in confidence -- where the real crisis lies. In the meantime, we expect sharp bouts of bargain hunting and more panic sell-offs."

In Iceland, Prime Minister Geir Haarde said the government was ready to take control of the country's banks, citing "a gargantuan crisis which is part of a broader worldwide crisis."

After a weekend summit of the European Union's big four leaders in Paris, member states' leaders issued a joint statement on Monday vowing to defend banks while remaining divided on a US-style bailout fund.

The turbulence pushed the euro down against the dollar and yen, while oil prices fell below 90 dollars a barrel on fears about slowing demand for energy.

{kind=link}

No comments:

Post a Comment